Why Most Crypto Futures Journals Fail

Most trading journals fail in crypto futures for one simple reason. They are built like spot trading journals. Futures trading is not just buying and selling with a different order type. It introduces leverage, liquidation, funding, and margin mechanics that completely change how risk works. If your journal does not account for those, it is not showing you the real story behind your results.

Many traders think they are journaling because they write down entry, exit, and profit. In futures, that is surface-level data. Two trades with the same profit can have completely different risk profiles. One might be a controlled 3x leverage position with wide liquidation distance. The other might be a 25x leverage gamble that survived by luck. If your journal treats them as equal, it is training you to misread your own performance.

This is why most futures traders either give up on journaling or end up with a bloated spreadsheet that never gets reviewed. The system is too slow, too complex, or missing the data that actually matters.

A proper crypto futures journal is not about writing more. It is about recording the right variables so you can see leverage exposure, liquidation risk, funding drag, and execution mistakes clearly. Once those are in place, journaling becomes fast and useful instead of exhausting.

This guide shows you how to build that system step by step.

What Makes a Crypto Futures Journal Different

A futures journal exists for one reason that spot journals do not have. It must help you understand how close you are to failure. In spot trading, the worst case is usually a drawdown that hurts emotionally or financially. In futures trading, the worst case is liquidation, which means total loss of margin on that position. Your journal should constantly show you how often you are flirting with that line.

Leverage changes everything about how a trade should be evaluated. A small move against you at 20x leverage is not the same as the same move at 3x. The chart looks identical, but the risk profile is completely different. When traders say their strategy is profitable but they still feel unstable, it is usually because leverage is hiding the real volatility of their account. A futures journal must separate results by leverage or it becomes blind to that risk.

Liquidation price is another futures-only variable that most traders ignore. You can be profitable and still be trading too close to liquidation. If your journal never shows how often price came within a few percent of wiping you out, you are missing one of the most important diagnostics available. A trade that finishes green but came dangerously close to liquidation is a warning sign, not a success.

Funding adds a slow leak that spot traders never experience. If you hold positions for hours or days, funding payments can quietly drag down performance. Over time, this changes which setups are truly profitable. A proper futures journal makes funding visible so you can see whether certain strategies only work before funding is applied.

Margin mode matters as well. Cross margin and isolated margin carry very different risk profiles. Cross margin can hide liquidation risk by spreading it across your account. Isolated margin makes it visible at the position level. Your journal should reflect which mode you are using so you can see how often you rely on your full balance to save bad trades.

All of this means a crypto futures journal is not just a record of trades. It is a risk exposure map. It shows how aggressively you are trading, how close you run to liquidation, how funding affects your edge, and whether your profits come from skill or from temporary survival. Without these variables, a futures journal becomes a simplified diary instead of a decision tool.

The Minimum Data Fields Every Futures Trade Must Have

If your journal does not capture futures-specific variables, it is not a futures journal. It is just a generic trade log with futures trades inside it. The goal here is not to collect everything. The goal is to collect what actually explains risk, stability, and repeatability.

Every futures trade should answer four questions:

How aggressive was I?

How close was I to liquidation?

How much did holding cost me?

Was this execution skill or survival?

That is what these fields are designed to expose.

You still need the basic structure:

Exchange

Pair

Direction (long or short)

Entry price

Exit price

Position size

Profit or loss

Those are non-negotiable. But in futures, they are only the outer shell.

The first futures-specific variable is leverage. Leverage defines how fragile the position is. Two trades with identical PnL but different leverage are not equal. One is stable, one is dangerous. If you never tag or record leverage, you are mixing completely different risk profiles into the same data pool.

Margin mode comes next. Isolated margin shows you exactly how much you were willing to lose. Cross margin hides risk inside your total balance. Without recording this, you cannot evaluate whether your strategy depends on account-level bailouts.

Liquidation price is one of the most important fields and also one of the most ignored. It shows how much room you actually gave the trade to breathe. A trade that survives by 1% before liquidation is not a clean execution. It is a warning.

Funding is the slow cost of futures trading. If you hold positions through multiple funding intervals, those payments can completely change expectancy. A journal that shows raw PnL without funding is lying to you over time.

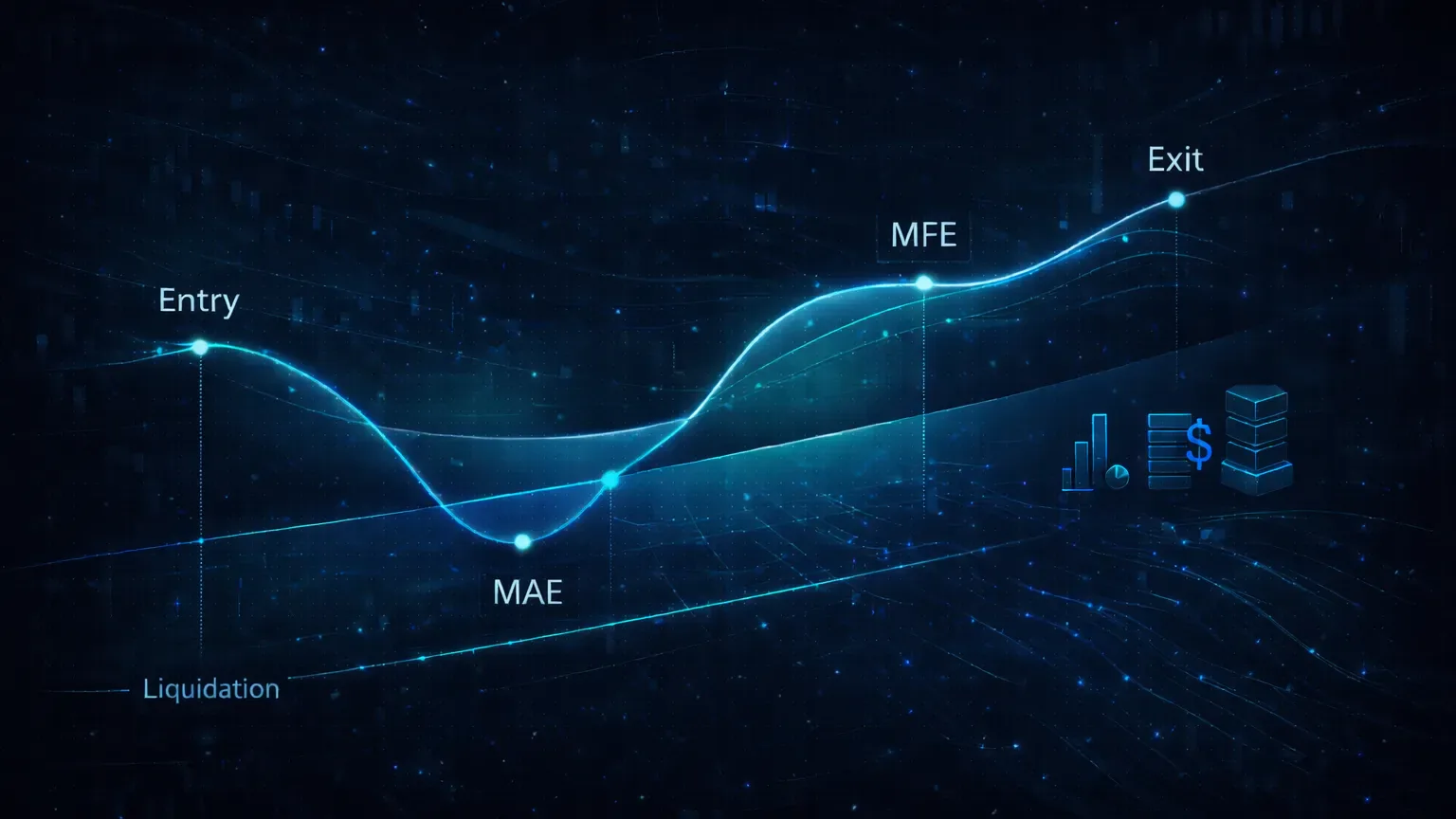

MAE and MFE complete the risk picture:

MAE (Maximum Adverse Excursion) shows how far price went against you.

MFE (Maximum Favorable Excursion) shows how much profit was available.

Together, they show whether your entries are precise and whether you exit too early or too late.

Session or market context adds one more layer. London, New York, Asia, news volatility, low liquidity periods. Over time, patterns emerge here that most traders never notice.

| Field | Why It Matters |

|---|---|

| Exchange | Execution quality, liquidity, and funding vary by platform |

| Pair | Different pairs have different volatility profiles |

| Direction | Long and short performance often differs |

| Entry Price | Base reference for all risk and reward metrics |

| Exit Price | Determines realized outcome |

| Position Size | Shows real exposure, not just percentage risk |

| Leverage | Defines fragility of the position |

| Margin Mode | Reveals whether risk was isolated or account-wide |

| Liquidation Price | Shows true failure point of the trade |

| Funding Paid/Received | Shows holding cost or benefit |

| Fees | Impacts net profitability |

| MAE | Shows how close the trade came to invalidation |

| MFE | Shows whether profit potential was fully captured |

| Session / Context | Helps identify time-based performance patterns |

Notice what is missing. There is no room for emotional essays. There is no need for dozens of custom fields. The purpose is not to describe how you felt. The purpose is to diagnose how you traded.

If you capture these fields consistently, you gain three powerful filters:

You can separate results by leverage and instantly see if higher leverage actually improves returns or just increases stress.

You can scan liquidation distance to see how often you are trading on the edge of account failure.

You can measure funding drag to know whether your strategy only works before costs are applied.

This is the foundation that turns journaling from memory keeping into risk analysis.

What a “Perfectly Journaled” Futures Trade Looks Like

Abstract fields only become useful once you see how they work together in a real trade. A properly journaled futures position should read like a compact risk profile, not a story. When you look at it, you should instantly understand how aggressive the trade was, how close it came to failure, and whether the outcome was skill or luck.

Imagine this example:

You take a BTCUSDT long on Binance at 42,000 using 10x leverage with isolated margin. Your position size is $2,000, which means your actual margin at risk is $200. Your liquidation price is 38,100. That already tells you something important. You allowed roughly a 9.2% move against your entry before total loss.

Price moves against you first and hits 41,300 before reversing. That becomes your MAE. You were about 1.7% from liquidation at the worst point of the trade. Even if the trade later wins, this is a critical piece of information because it shows how tight your margin for error was.

Price then moves in your favor and reaches 43,200 before you exit at 42,800. That 43,200 level becomes your MFE. It shows how much profit was available versus how much you actually captured. If this pattern repeats across trades, it tells you something about your exit discipline.

You hold the position for six hours and pay a small funding fee. That fee slightly reduces your net PnL. Over dozens of similar trades, this becomes a measurable cost that might change which setups are worth trading.

| Field | Value |

|---|---|

| Exchange | Binance |

| Pair | BTCUSDT |

| Direction | Long |

| Entry Price | 42,000 |

| Exit Price | 42,800 |

| Position Size | $2,000 |

| Leverage | 10x |

| Margin Mode | Isolated |

| Liquidation Price | 38,100 |

| MAE | 41,300 |

| MFE | 43,200 |

| Funding | -$1.20 |

| Fees | -$2.80 |

| Net PnL | +$35.50 |

| Session / Context | New York session, moderate volatility |

| One-line Note | Entry slightly early, exit cautious after funding |

When you look at this trade, you immediately see:

You risked a full liquidation for a relatively small gain.

You came dangerously close to your liquidation price before price reversed.

You captured only a portion of the available move.

Funding and fees meaningfully impacted a modest win.

This is what makes a futures journal powerful. The trade does not just say “+35 dollars.” It shows the structure behind that number. It exposes whether the trade was efficient, risky, or barely survived.

A “perfectly journaled” trade is not perfect because it made money. It is perfect because it contains everything needed to evaluate whether it should be repeated.

How to Journal a Futures Trade in Under 60 Seconds

Speed is what makes journaling sustainable in futures. If logging a trade takes five minutes, you will skip it. If it takes one minute, you will do it even on busy trading days. The system must be designed so that most of the data is captured automatically and only the decision-critical parts are added manually.

The moment a trade closes, the technical data should already exist. Entry, exit, position size, leverage, margin mode, fees, funding, and liquidation price should be pulled directly from the exchange. This is not a convenience feature. It is a requirement. Manual entry here introduces errors and friction, which eventually kills consistency.

Your manual work is limited to three actions:

First, tag the trade. This usually means leverage category, setup type, and any major mistake if one occurred. High leverage trades should be easy to filter later. Mistakes should be standardized so patterns can form.

Second, glance at liquidation distance. You do not need to calculate anything. Just ask one question. Did this trade ever come uncomfortably close to liquidation? If yes, that is a risk flag even if the trade was profitable.

Third, write a one-line execution note. One sentence only. Something like:

“Entry slightly late, risk too tight.”

“Good entry, exit cut early because funding.”

“Overleveraged due to FOMO.”

That is enough. You are not writing a diary. You are marking diagnostics.

If your process requires more than this, it is too heavy. Futures traders often place many trades in a session. The journal must respect that reality. Automation handles the numbers. You handle the interpretation.

This is where a crypto-native journal like TradeChainly quietly changes behavior. When trades are imported automatically and liquidation, leverage, and funding are already visible, journaling becomes a short review action instead of a data entry task. That is what allows you to journal every trade without burning out.

The mental model is simple. Capture first. Analyze later. Speed protects consistency, and consistency is what turns data into edge.

Daily Futures Journaling Workflow

Your daily workflow is where journaling either becomes automatic or gets abandoned. The goal is not deep analysis. The goal is to create clean, reliable data with minimal effort so that your weekly review actually means something.

Start by importing your trades. This should happen without any manual input. Whether you traded one position or thirty, they should already be waiting for you in your journal when the session ends. If this step is manual, everything else becomes optional in practice.

Once trades are in, scan through them and apply your core tags. Leverage is the first one. Separate low, medium, and high leverage trades. Over time, this alone will tell you whether higher leverage is helping or hurting your results.

Next, tag any obvious execution mistakes. Keep this list short and consistent. Things like late entry, no stop plan, overleveraged, emotional entry, or chasing price. The power of tags comes from repetition, not from creativity.

Then check liquidation proximity. You are not doing math here. You are simply asking whether price came uncomfortably close to the liquidation level. If it did, that is information worth remembering even if the trade closed green.

Finish with your one-line note. One sentence that captures the most important execution insight from the trade. Not a story. Not an emotion dump. Just the technical lesson.

This entire process should take only a few minutes per day. If you feel resistance to opening your journal, it usually means you are trying to analyze too early. Daily journaling is about labeling, not judging. The judgment comes later when patterns exist.

Weekly Futures Review Workflow

The weekly review is where your journal becomes a decision tool. Daily journaling creates clean data. Weekly review turns that data into adjustments you can actually trade.

Start by filtering your trades by leverage. Look at low leverage, medium leverage, and high leverage separately. Do not mix them. Most traders discover something uncomfortable here. Their highest leverage trades usually carry the most emotional pressure and the worst risk efficiency. Even when they are profitable, they often show lower consistency and higher liquidation proximity. This is where you decide whether high leverage is adding edge or just amplifying variance.

Next, review liquidation distance. Go through your trades and identify how often price came close to liquidation. You are looking for patterns, not isolated events. If a large percentage of your trades survive within a narrow buffer from liquidation, your strategy is structurally fragile even if your PnL looks positive. That means one bad sequence could wipe weeks of progress.

Now look at funding. Filter trades by holding time and funding paid or received. You might find that certain setups only work before funding is applied. Others might look fine on the chart but lose profitability once funding costs are included. This is especially important for traders who hold futures positions overnight or for multiple days.

After that, scan your mistake tags. This is where behavioral patterns show up. Late entries, overleveraging, skipping stops, or revenge trades will usually cluster. You are not looking for perfection. You are looking for repetition. One repeated mistake matters more than ten random ones.

Finally, review MAE and MFE together. MAE shows how wrong your timing was. MFE shows how much you left on the table. If MAE is large and MFE is small, your entries are weak. If MAE is small and MFE is large but your exits are early, your management needs work. This is one of the most powerful diagnostic pairs in futures journaling.

The outcome of a weekly review should be simple. One or two concrete adjustments. Lower leverage on certain setups. Wider invalidation on others. Avoiding specific sessions. You are not rewriting your strategy. You are tuning risk.

The Most Common Futures Journaling Mistakes

Most futures journals fail not because traders lack discipline, but because the system is built wrong from the start. The mistakes are structural, and once they are in place, journaling becomes either misleading or exhausting.

The first mistake is tracking too many fields. More data does not mean more clarity. When traders create journals with twenty or thirty custom inputs, they stop filling them out after a few days. A futures journal only needs what explains risk and execution. Everything else becomes noise.

The second mistake is not separating trades by leverage. If 3x and 25x trades live in the same dataset, your statistics become meaningless. Your win rate, expectancy, and drawdowns are now averages of completely different risk profiles. This hides whether your edge comes from controlled execution or from aggressive exposure.

The third mistake is ignoring liquidation entirely. Many traders know their liquidation price when entering a trade, but they never record it or review how close price came to it. That is like driving a car without checking how often you almost crashed. Liquidation proximity is one of the strongest signals of structural risk in futures trading.

Another common error is treating notes like therapy. Journals filled with emotional paragraphs feel productive but rarely improve execution. Notes should describe what happened technically, not how the trade felt emotionally. “Overleveraged due to FOMO” is useful. A full page about frustration is not.

Finally, many traders rely on manual-only systems. Spreadsheets and notebooks seem flexible, but they break under futures volume. When data entry becomes work, journaling becomes optional. Optional systems do not survive long-term.

A futures journal should feel light, not heavy. If it feels heavy, something is wrong with the structure, not with your discipline.

Why Automation Is Mandatory for Futures Journaling

Manual journaling collapses in futures trading because of volume and complexity. A spot trader might place a few trades per week. A futures trader can place several in a single session. Each one carries leverage, funding, margin mode, liquidation price, and fees. Asking yourself to manually type all of that is not discipline. It is friction disguised as responsibility.

Friction always wins in the long run. The more effort a system requires, the more selective you become about using it. You skip small trades. You delay entries. You forget details. Over time, the journal becomes incomplete, and incomplete data is worse than no data because it creates false confidence.

Automation removes that failure point. When trades are synced directly from the exchange, every position exists in your journal whether you feel motivated or not. Entry, exit, size, leverage, funding, fees, and liquidation price become facts instead of manual tasks. That shifts journaling from data entry to interpretation.

Halfway through a session, you should already know that your journal is forming itself in the background.

This is where crypto-native tools quietly change behavior. A platform like TradeChainly does not make you journal better by forcing habits. It makes journaling easier by making the data unavoidable. When your trades are always there, reviewing them stops being a chore and starts being part of trading.

Automation also protects accuracy. Funding, fees, and liquidation prices are often calculated incorrectly in manual systems. Small errors compound into misleading statistics. A futures journal is only useful if the numbers reflect reality.

If your journal depends on motivation, it will fail. If it depends on automation, it becomes infrastructure. That difference decides whether your data survives long enough to teach you anything.

Turn Your Journal Into a Risk Management System

A crypto futures journal is not about documenting trades. It is about controlling risk in an environment where risk compounds fast. Leverage, liquidation, and funding turn small mistakes into account-level damage. Your journal exists to make those forces visible before they hurt you.

When your journal captures the right data, the work becomes simple. You see which leverage levels you handle well. You see how often you trade too close to liquidation. You see whether funding quietly eats your edge. And you see whether your profits come from clean execution or from survival.

Consistency matters more than perfection. A fast system that you use every day will always outperform a perfect system that you avoid. That is why automation and structure are not optional in futures journaling. They are the foundation that keeps your data honest.

If you want a journal that handles the technical complexity of futures trading without slowing you down, this is exactly what a crypto-native platform like TradeChainly is built for. Not to replace your thinking, but to remove friction so your data is always ready when you need it.

Your journal should not feel like homework. It should feel like a safety system. When it does, it becomes one of the most valuable tools in your trading.