Why Do Futures Trading Mistakes Stay Hidden for So Long?

If you trade crypto futures long enough, you get used to losses that feel random. One day the market chops you up. The next day volatility spikes and wipes out two days of gains. It is easy to blame conditions, funding, or bad luck and move on.

The problem is that most futures trading mistakes do not feel like mistakes in real time.

Trading leveraged perpetuals in a 24/7 market moves fast. You enter, manage risk, adjust size, maybe re-enter. By the end of the session, all you remember is the net result. The specific decisions that caused that result are already blurred together. Your brain keeps the narrative simple. The market was messy. Liquidity was thin. BTC chopped. Funding flipped. You did what you could.

That’s how repeatable errors survive.

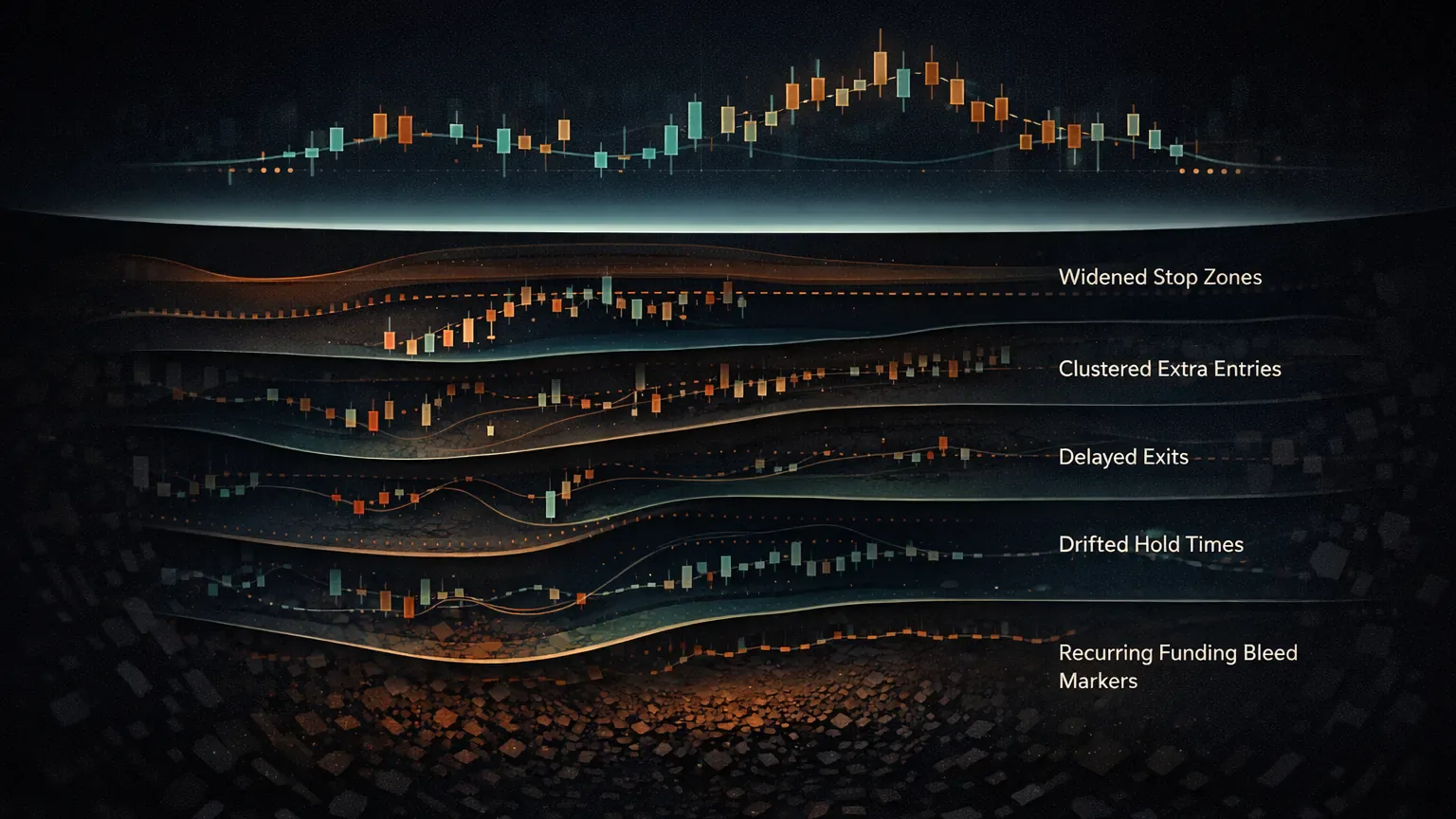

Most execution mistakes are small on their own. Slightly wider stops during volatility. One extra trade during chop. Holding a position through funding when the setup was already invalid. None of these feels dramatic. But over dozens or hundreds of trades, they quietly shape your equity curve.

Memory-based review makes this worse. You remember the emotional trades and the big losses. You forget the subtle behaviors that drain expectancy. Without aggregated data, every losing stretch feels unique, even when it is caused by the same few patterns repeating.

That’s why many futures traders believe they are disciplined while their results say otherwise. The mistakes are there. They are just invisible without structure.

What Does Fixing It Look Like in Practice?

Consider a trader who trades SOL and MATIC perpetuals on OKX intraday. On the surface, their stats look fine. Win rate sits around 48–52%. Average winner is slightly larger than average loser. Nothing screams failure. Yet month after month, the account drifts lower.

Before journaling, the explanation is vague. Market conditions changed. Volatility is different. Too many fake breakouts.

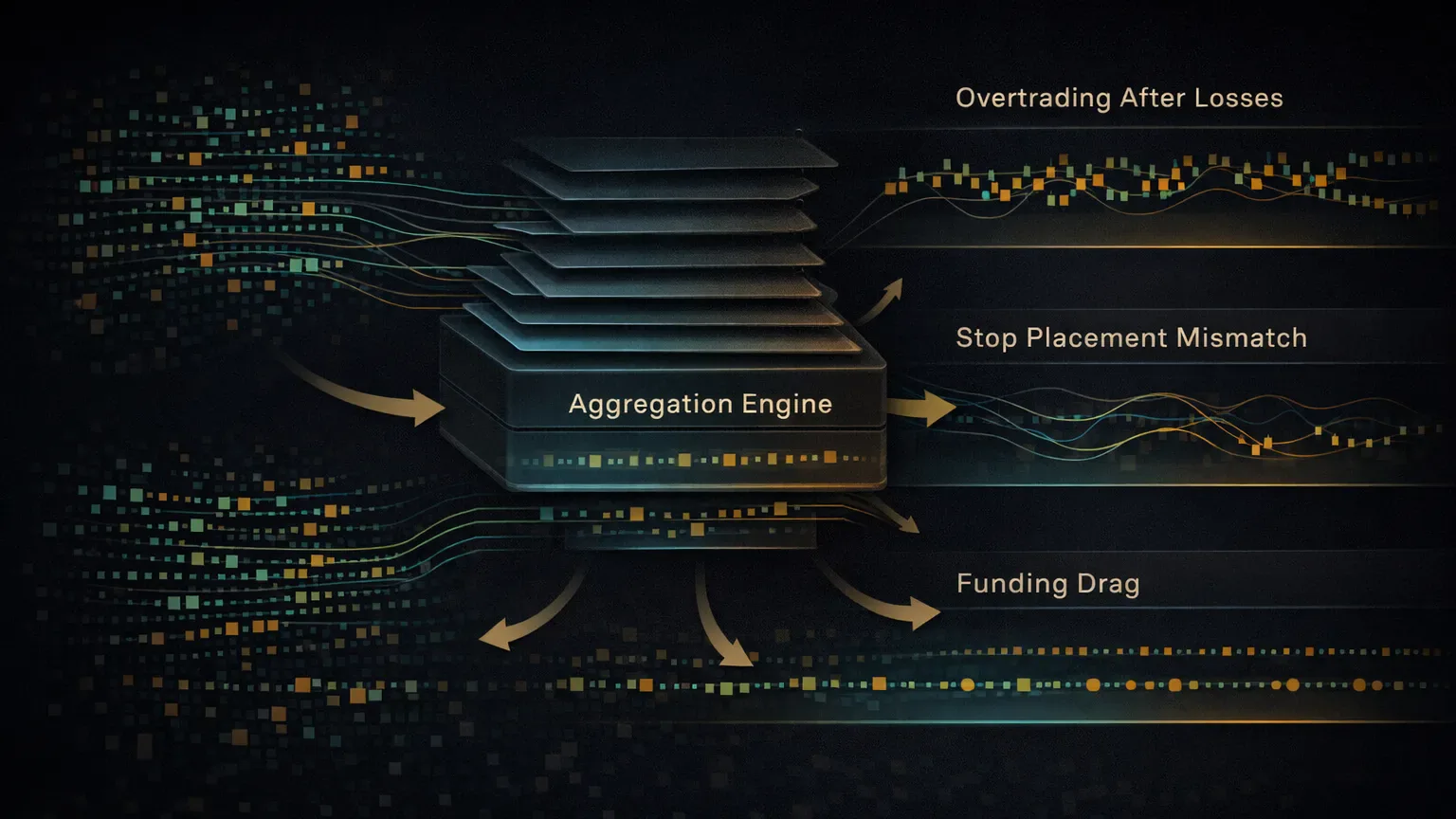

Once the trades are reviewed in aggregate, the real issues surface quickly.

The first problem is trade frequency. On red days, the trader takes almost twice as many trades as on green days. Most of those extra trades happen after the first loss. They are not reckless, but they are rushed. Entries are closer together. Confirmation is weaker. Expectancy on these trades is sharply negative.

The second issue appears in MAE and MFE data. Many losing trades would have worked with slightly wider stops. At the same time, many winning trades show high MFE followed by early exits. The trader is absorbing volatility inconsistently and failing to capitalize when price actually moves.

The third leak is funding. A surprising portion of losses comes from trades held longer than planned. These positions do not expand. They drift. By the time they close, funding has eaten most of the edge. This is especially noticeable on overnight holds and weekends.

None of these issues felt obvious while trading. Together, they explain the entire drawdown.

The fixes are not dramatic. The trader caps trades per session. Implements a mandatory break after two consecutive losses. Adjusts stop placement based on observed MAE instead of fear. Adds a time-based exit rule to avoid paying unnecessary funding.

Over the next 30 days, win rate barely changes. What changes is behavior. Trade count drops. Average loss shrinks. Funding paid is cut in half. The equity curve stabilizes, not because of a new strategy, but because old mistakes are no longer allowed to repeat unchecked.

Why Does Journaling Turn “Bad Trades” Into Patterns?

The moment you start journaling futures trades properly, the story changes. Not because you suddenly trade better, but because your mistakes stop hiding.

Instead of looking at trades one by one, you begin to see them in groups. The narrative shifts from “that trade didn’t work” to “this keeps happening under the same conditions.” Futures trading mistakes are rarely isolated events. They are behaviors that repeat across sessions, symbols, and market regimes.

A journal forces aggregation. Trade count by session. PnL by time of day. Win rate by tag. Average holding time on losers versus winners. Funding paid per trade. When you see these metrics side by side, excuses lose their power. The data does not care how confident you felt in the moment.

This is especially important in crypto futures because leverage amplifies small errors. A tiny timing issue or an extra entry can flip a green day red once fees, funding, and slippage are included. Without journaling, those costs are invisible. With it, they show up as clear statistical fingerprints.

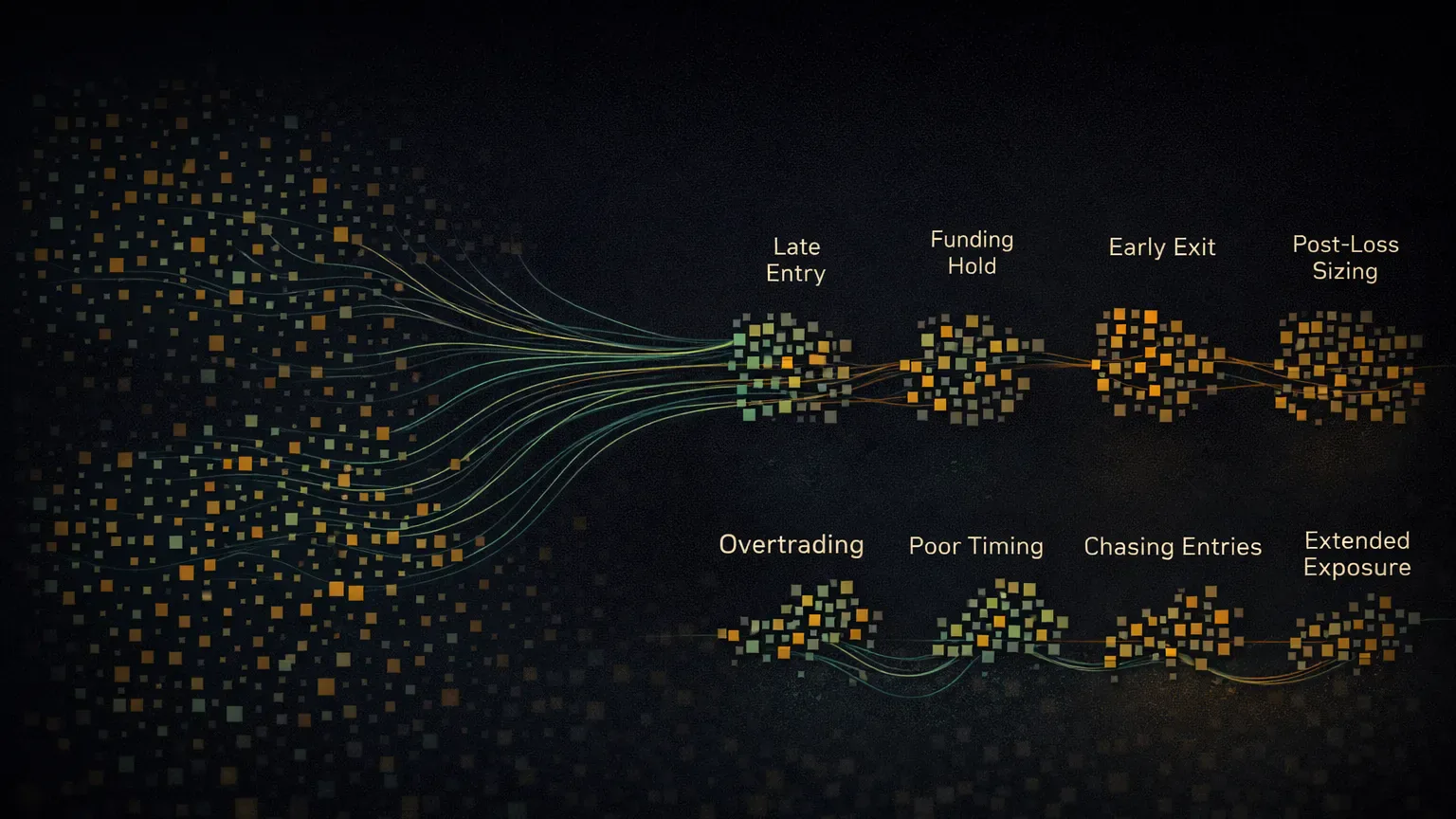

Another shift happens when you stop labeling mistakes emotionally and start labeling them behaviorally. Instead of writing “bad trade” in your notes, you tag what actually happened. Overtraded during chop. Late entry after impulse. Held through funding without edge. Scaled size after a loss. These labels turn vague frustration into something measurable.

Over time, patterns emerge that you could never spot in real time. The same type of mistake shows up in different market conditions. The same execution error clusters around the same hours or symbols. Journaling does not judge those patterns. It simply exposes them.

Seeing it that clearly is what makes improvement possible.

When Is “Being Active” Just Overtrading?

Overtrading in crypto futures rarely feels reckless. Most of the time, it feels productive. You are at your desk. Volatility is there. Setups look close enough. You are engaged. From the inside, it feels like you are doing your job.

Your journal says otherwise.

When you review trade count against performance, overtrading becomes obvious. PnL flattens or turns negative as trade frequency increases. Win rate stays roughly the same, but expectancy drops. Fees and funding begin to dominate the results. The edge you thought you had gets diluted by volume.

This pattern shows up clearly in session data. Choppy conditions produce more trades, not better ones. Instead of waiting for clean setups, you take marginal entries just to stay involved. Individually, each trade looks defensible. In aggregate, they form a cluster of low-quality decisions.

Crypto futures make this worse because the market never closes. There is always another candle, another micro move, another reason to click. Journaling exposes how often “just one more trade” turns into five. It also shows when those trades happen. Late sessions. After an early loss. During low-liquidity hours. On weekends when spreads widen and follow-through fades.

Once you tag overtrading as a mistake, patterns sharpen further. You see which symbols trigger it. Which sessions invite it. Which emotional states correlate with it. The issue is no longer self-control in the abstract. It becomes a specific behavioral leak tied to measurable conditions.

Fixes get practical here. Trade caps per session. Hard stops after consecutive losses. Time-based rules during chop. None of these come from discipline alone. They come from seeing the damage clearly enough to act.

What Do MAE and MFE Reveal About Your Stops?

Stop placement mistakes are some of the hardest to diagnose without data. In the moment, your stop almost always feels reasonable. It is based on structure, volatility, or risk limits. When it gets hit, the explanation is ready. The market was noisy. A sweep happened. Liquidity hunted the level.

Data cuts through that narrative.

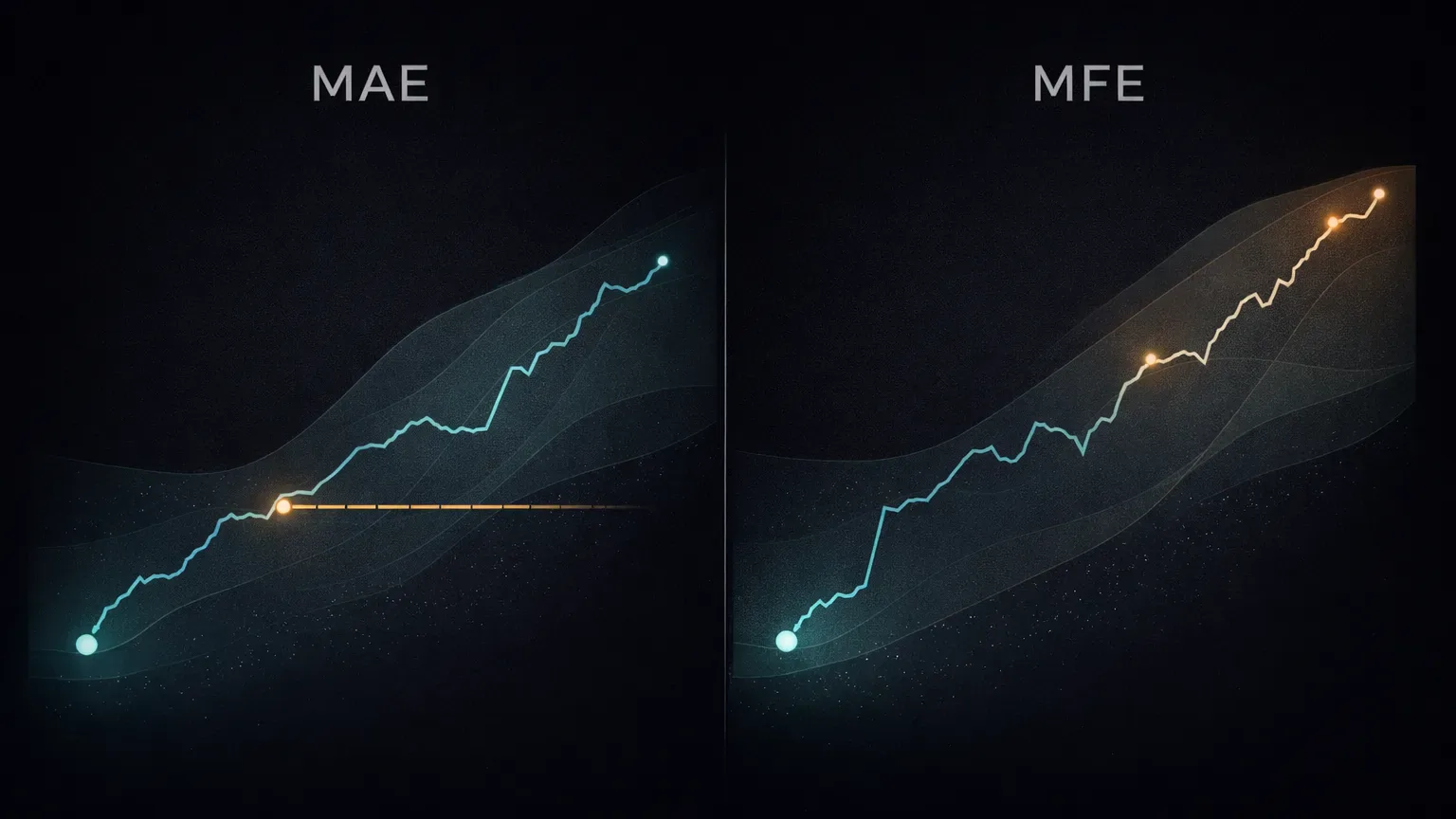

When you review maximum adverse excursion (MAE) across your trades, patterns start to surface. You notice how often price moves slightly against you before going in your intended direction. If a large percentage of your losing trades have small MAE values, it usually means your stops are too tight for the volatility you are trading. You are not wrong on direction. You are wrong on tolerance.

This becomes even clearer when you compare MAE on losers to MAE on winners. Many futures traders discover that their winning trades regularly absorb more heat than their losing ones. That is a red flag. It suggests inconsistency in execution, often caused by fear of liquidation or recent losses influencing stop placement.

Midway through reviewing this data, another metric adds context.

Maximum favorable excursion (MFE) shows how much profit was available before exit. When you see high MFE values paired with early exits, a different mistake emerges. You are surviving volatility but failing to capitalize on it. This is common in crypto futures, where sharp impulses are often followed by shallow pullbacks. Traders who exit at the first reaction miss the core move repeatedly.

Journaling also reveals where these stop issues cluster. High-volatility sessions. News-driven moves. Certain symbols with thinner books. What feels like random stop-outs often turns out to be the same mismatch between volatility and risk parameters, repeated again and again.

Once you see this in the data, the solution becomes specific. Wider stops with smaller size. Volatility-adjusted risk. Different rules for different sessions. These adjustments are not theoretical. They are responses to patterns your own trades have already exposed.

How Do You Spot Revenge Trading When It Feels “Controlled”?

Most traders think revenge trading is obvious. Slamming size after a big loss. Jumping into a random setup out of frustration. Losing control. In reality, the most damaging revenge trading in crypto futures is subtle.

It often looks calm from the outside.

You take a loss. Then another. Instead of stepping away, you keep trading. Position size stays the same, or even decreases slightly. Setups still look valid. Nothing feels emotional enough to raise alarms. But the journal tells you this sequence behaves very differently from your baseline trades.

When you review loss clusters, revenge trading shows up as compressed timing. Trades taken closer together than usual. Reduced patience between entries. Less time spent waiting for confirmation. You may also see a drop in average trade quality right after red trades, even though the setups are tagged the same.

Time-of-day data sharpens this further. Many traders discover that their worst performance happens in narrow windows following losses. Fifteen minutes. Thirty minutes. One hour. These windows repeat across weeks and months. The market changes. The behavior does not.

Another giveaway is size behavior. Some traders increase size after a loss to “make it back.” Others do the opposite and reduce size while continuing to trade, trying to grind back slowly. Both are forms of revenge trading. The common factor is not aggression. It is refusal to reset.

Crypto futures make this especially dangerous because opportunities never stop. There is always another setup forming. Without journaling, it feels rational to keep trading. With journaling, you see how often those post-loss trades drag down otherwise profitable days.

Once identified, this mistake becomes manageable. Cooling-off rules. Mandatory breaks after consecutive losses. Session limits triggered by behavior, not emotion. Journaling does not shame you for revenge trading. It shows you exactly when it happens and how much it costs.

Where Does Funding Quietly Eat Your Edge?

Funding rates are one of the most overlooked leaks in crypto futures trading. They rarely feel like mistakes because they are small, gradual, and easy to ignore during a single trade.

The problem is that funding does not show up clearly in trade memory. You remember entries and exits. You remember price. You do not feel the slow bleed of paying funding every eight hours while holding a marginal position.

Journaling makes this visible.

When you review holding time alongside PnL, patterns start to emerge. Trades held longer than your core setup requires often underperform, even when they eventually close green. Once funding is included, many of those trades flip negative. This is especially common for traders with a directional bias who hold longs during periods of positive funding or shorts during negative funding, assuming price movement will compensate.

The journal exposes this by aggregating funding paid by tag, symbol, or session. You see which types of trades quietly lose money even when your read is decent. Weekend holds. Overnight positions. Trades that drift instead of expand. These are not strategic swing trades. They are execution mistakes disguised as patience.

Crypto futures markets amplify this issue because funding environments can persist for days or weeks. A small edge disappears when you repeatedly pay to stay in trades that no longer have momentum. Without data, this feels like bad luck. With data, it becomes a clear behavioral leak.

Once identified, the fix is straightforward. Tighter time-based exits. Explicit rules for holding through funding. Separate tagging for “extended holds” versus core intraday trades. Journaling turns funding from an afterthought into a decision variable you actively manage.

What Does This Look Like Inside a Journal, Day to Day?

Seeing mistakes is only useful if you can act on them consistently. This is where journaling workflows matter more than insight alone.

Effective futures journals separate setups from mistakes. A trade can follow a valid setup and still include an execution error. Tagging those errors is what turns awareness into accountability. Overtrading, late entries, early exits, holding through funding, poor stop placement. These tags let you measure behavior directly, not just outcomes.

Session-level review adds another layer. Instead of asking whether you made money, you look at how you traded. Trade count versus plan. Time between trades. PnL before and after the first loss. These views make it obvious when discipline slipped, even on green days.

Notes play a different role once data is in place. Instead of emotional venting, notes capture context. Why you entered. Why you stayed longer than planned. Why you ignored a rule. Over time, these notes explain the numbers. They show how mental state and market conditions interact with execution.

Automation matters once you are serious about consistency. When trades are imported automatically and metrics update continuously, review becomes frictionless. You are not relying on memory or incomplete records. You are responding to what actually happened. Tools like TradeChainly exist to make this process sustainable, not to replace thinking, but to support it with accurate data.

A good workflow does not aim for perfection. It aims to make repeating the same mistake harder each week than the last.

How Do You Turn Awareness Into Fewer Red Days?

Spotting mistakes in your journal feels satisfying, but insight alone does not change results. What actually reduces red days is turning those observations into constraints that shape how you trade going forward.

The shift happens when you stop asking, “What went wrong?” and start asking, “What am I no longer allowed to repeat?” Journaling gives you the evidence to answer that honestly. If overtrading consistently drags your expectancy down, the solution is not trying to feel more patient. It is setting a hard trade cap per session. If post-loss trades underperform, the fix is a mandatory pause after consecutive losses, not better motivation.

These rules work because they are grounded in your own data. They are not borrowed from a trading book or a Twitter thread. They exist because your journal has already proven what hurts your performance. That makes them easier to respect, even on difficult days.

Another important shift is measuring success differently. Fewer red days do not come from forcing more green days. They come from limiting damage when conditions are not there. Journaling shows you which behaviors turn small losses into large ones. When those behaviors are constrained, drawdowns compress naturally.

Over time, this process compounds. Mistakes do not disappear overnight, but they lose influence. The same error that once cost you a full day now costs a fraction. The same setup that used to spiral into revenge trading now ends with a controlled stop and a break.

That is the real value of journaling for crypto futures traders. It does not make markets easier. It makes your own weaknesses visible, measurable, and progressively less expensive.