Cutting the Hidden Fee Leak

Trade well for weeks and still feel like something is off.

Executions are clean. Entries make sense. You catch good intraday moves, especially during high-volume windows. When you scroll through your trades, most of them are green. Yet when you look at your account balance, progress feels slow, inconsistent, or flat.

That frustration shows up constantly for active crypto day traders, and it gets misdiagnosed all the time.

The issue is rarely strategy selection. It is almost never “you need a better setup.” More often, it is an invisible performance leak that only shows up when you look at your data the right way.

Fees.

Not in the obvious sense of “fees exist.” Everyone knows exchanges charge fees. The problem is how fees quietly distort your perception of profitability. They reshape your edge without showing up clearly in your day-to-day decision-making.

Most traders evaluate performance using gross outcomes. Win rate. Average win. Average loss. Total PnL before costs. On paper, those numbers can look solid. In reality, they are incomplete. Fees sit between your execution and your actual account growth, compressing results trade by trade.

Crypto day trading amplifies this distortion. You are operating in a 24/7 market. You trade more frequently. You often work with smaller targets and tighter stops. You cross the spread more often in fast conditions. All of that means fees are not a background cost. They are an active variable in your edge.

Fees also do not announce themselves as the problem. You do not see them as a single large loss. You see them as friction. A few dollars here. A few dollars there. Over dozens or hundreds of trades, that friction becomes structural drag.

This is why so many traders say, “My strategy works, but my account doesn’t grow.”

What they are really saying is this: their gross performance suggests an edge, but their net performance tells a different story.

Until you isolate how fees affect your metrics, you are evaluating your trading through a distorted lens. You are making decisions based on numbers that do not reflect reality.

That is what this article is about. Not why fees exist, but how they quietly reshape your edge and how to see that distortion clearly in your data.

The Fee Problem in Crypto Day Trading

If you trade crypto intraday, fees are not just a line item. They are embedded into the structure of how you trade.

Most day traders operate with relatively tight margins. You are not holding for multi-day moves where fees fade into the background. You are targeting small-to-moderate price movements, often measured in fractions of a percent. When your average win is close to your average loss, costs matter more than most traders want to admit.

Frequency is the first multiplier. A swing trader might take five to ten trades a month. A crypto scalper can take that many in a single session. Even at competitive fee tiers, those costs compound quickly. What looks negligible on one trade becomes meaningful over a sample of 200 or 300.

Execution style makes this worse. In fast-moving crypto markets, especially during news-driven volatility or liquidation cascades, many traders end up paying taker fees. You hit the market to get filled. You prioritize execution over price. That decision makes sense tactically, but it increases your effective cost per trade.

Then there is the spread. On paper, you might be paying a low taker fee. In practice, you are also crossing a wider spread during high volatility or low-liquidity windows, such as late weekends or during sudden momentum bursts. That hidden cost behaves like an extra fee layered on top of the exchange charge.

Funding rates add another dimension. Futures and perpetual traders often ignore funding when reviewing intraday performance, especially if they do not hold positions long. But even short holds can be affected during aggressive funding periods. When you are trading frequently, funding becomes another recurring drag that chips away at net results.

Exchange structure matters too. Fee tiers, maker rebates, and liquidity profiles differ between Binance, Bybit, OKX, Coinbase, and others. A strategy that performs fine on one exchange can underperform on another purely because of cost structure and execution differences. Many traders do not notice this because they never isolate fees by venue.

What matters is not that fees are “high.” It is that crypto day trading magnifies their impact. High trade frequency, small targets, aggressive execution, and perpetual funding all combine to make fees a core part of your edge, not a secondary detail.

If you do not treat fees as a first-class performance variable, you end up diagnosing the wrong problems. You adjust entries. You tweak stops. You abandon strategies that may actually be viable once costs are properly accounted for.

Before you can improve execution, you need to understand how much of your performance is being shaped by costs you are not actively tracking.

Turning a Real Month Into a Reality Check (Case Study, Part 1)

Consider a common crypto scalping setup.

A trader focuses on high-momentum breakouts during the London and New York overlap. Trades are short. Targets are tight. The goal is consistency, not home runs. Over a month, the trader takes around 220 trades across BTC and ETH perpetuals.

On the surface, the stats look encouraging. The win rate sits at 56 percent. Average win is slightly smaller than average loss, but the high hit rate offsets it. Gross PnL for the month is positive. The trader feels like they have finally found something that works.

Then the numbers get reviewed more carefully.

How Fees Warp Your Metrics

Fees do not just reduce your bottom line. They change how your performance metrics behave, often in ways that are easy to miss if you only look at surface-level stats.

Start with win rate. A trade that closes slightly green before fees can easily flip to red after costs. When this happens across many trades, your effective win rate is lower than what your trade list suggests. You think you are winning 55 percent of the time. Net of fees, you might be closer to 48 or 49. That difference matters more than most traders realize, especially when evaluating consistency.

Expectancy is where the distortion becomes more dangerous. Expectancy is supposed to tell you whether your strategy has a positive edge over time. But expectancy calculated on gross results can be misleading in high-frequency environments. Small average wins get compressed by fees. Average losses usually do not shrink in the same way. The result is a strategy that looks slightly positive on paper but is negative after costs.

This compression is especially visible in scalping strategies. If your average win is 0.4R and your average loss is -1R, fees take a disproportionate bite out of the winners. A few dollars in fees might reduce your average win by 20 or 30 percent, while barely affecting the loss side. Over a large sample, that skew quietly pushes expectancy toward zero or below.

R-multiples suffer from a similar issue. Many traders review performance by looking at R distributions and assume that anything above breakeven is acceptable. But R calculations that ignore fees overstate performance. A trade that looks like a 0.2R winner before costs might be a negative R trade once fees are applied. When those marginal trades make up a large portion of your sample, your edge erodes without any obvious red flags.

This is why “breakeven” strategies bleed. On paper, they hover around zero. In reality, fees turn them into consistent losers. The trader feels like they are doing everything right. The data, once adjusted for costs, tells a different story.

The most misleading metric of all is total PnL without context. A green month does not mean a good strategy if fees are eating a large percentage of gross gains. Without seeing net performance alongside trade frequency and cost per trade, it is impossible to judge efficiency.

Fees do not show up as a single problem trade. They show up as statistical pressure. They flatten equity curves, compress distributions, and blur the line between skill and noise.

Until you look at your metrics after fees, you are not measuring your true edge. You are measuring a hypothetical version of your trading that does not exist in the real market.

What the Numbers Reveal Once Costs Are Counted (Case Study, Part 2)

Once fees are separated and applied trade by trade, the picture changes. Most entries are taker fills due to speed and volatility. Average fee per trade is not large, but it is consistent. Funding is neutral overall, but not zero.

After costs, the effective win rate drops to just under 50 percent. Many of the smallest winners flip to small losers. Expectancy turns slightly negative. The equity curve that looked smooth on a gross basis now shows slow decay.

Nothing about the strategy logic changed. Entries were still valid. Exits were still disciplined. The edge simply was not large enough to overcome execution costs at that frequency.

This is the uncomfortable middle ground many traders find themselves in. They are not randomly trading. They are not overleveraged. They are executing a coherent plan. But the plan operates too close to the fee boundary.

Building Fee-Aware Reviews from Your Journal Data

Seeing the impact of fees clearly requires more than just subtracting a number at the end of the month. It requires changing how you review your data.

Most traders lump fees into total PnL and move on. That approach hides patterns. What matters is how fees interact with specific behaviors: certain setups, certain sessions, certain execution choices. That only becomes visible when fees are treated as their own analytical layer.

A good starting point is separating gross and net performance. Gross results tell you whether your read of the market is directionally correct. Net results tell you whether that read is actually tradable at your current frequency and execution style. When those two diverge, fees are usually part of the explanation.

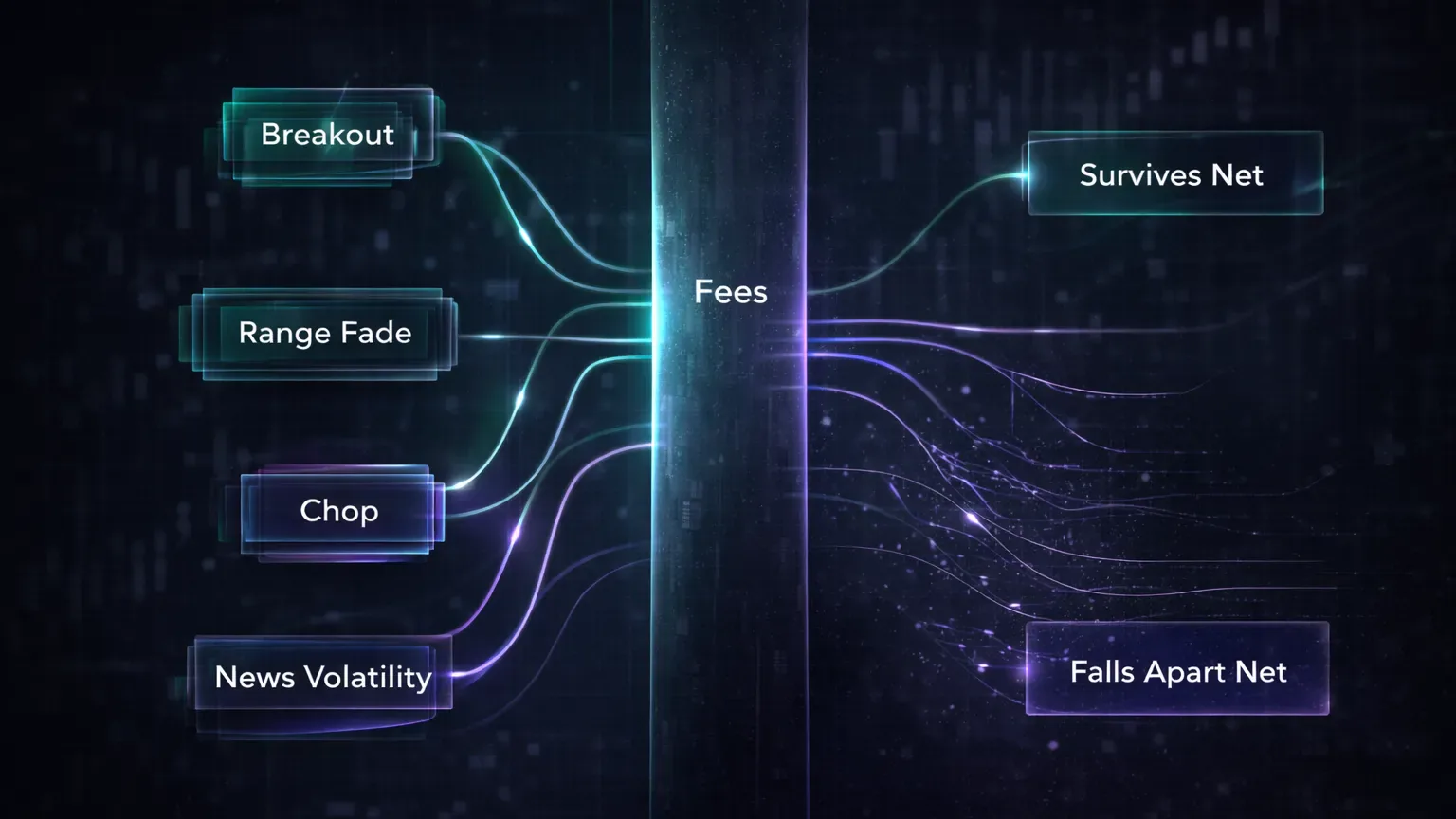

Once you have that separation, tagging becomes powerful. You can tag trades by setup, but also by context: breakout, range fade, chop, news volatility. When you review those tags net of fees, patterns emerge quickly. Some setups survive costs easily. Others look fine gross but fall apart once fees are applied.

MAE and MFE add another layer. If many of your trades barely clear fees before reversing, that tells you something about entry quality and timing. It often means you are trading too close to noise. Fees expose that weakness more clearly than price alone ever will.

Session-level analysis is another area where fees reveal hidden structure. Crypto trades differently across sessions. Weekend liquidity is thinner. Asia sessions can be slower and more range-bound. New York overlap brings speed and slippage. When you break down net results by session, you often find that certain windows are structurally fee-heavy, even if win rate stays high.

Automation matters here. Manually tracking fees across hundreds of trades is tedious and error-prone. A journal that continuously imports trades and includes fees in every metric makes this kind of review realistic. Inside TradeChainly, for example, fees are part of the trade record by default, which allows you to filter, tag, and report on performance without guessing or reconstructing data later.

The goal is not to obsess over every dollar paid to the exchange. The goal is clarity. Once you can see where fees hurt most, you can decide whether to adjust execution, reduce frequency, or drop certain trade types entirely.

Without that visibility, you are optimizing blind. With it, even small adjustments can materially improve net performance.

How Better Filters and Execution Protect Your Edge

Once fees are visible in your metrics, the fixes are usually more practical than traders expect. Most do not need a new strategy. They need cleaner execution and better filtering.

A common adjustment is raising the minimum quality bar for trades. When you review results net of fees, you often find a cluster of marginal trades that barely contribute to profit. They win just enough to feel productive but not enough to pay for themselves. Cutting those trades reduces activity but improves efficiency. Net PnL often stays the same or improves, even with fewer trades.

Execution style is another lever. Many traders discover that they default to taker orders even in conditions where patience would work. After seeing how much taker fees eat into small wins, they start experimenting with passive entries during slower periods. This does not mean forcing maker orders in fast markets. It means being selective about when speed is truly necessary.

Target sizing tends to change as well. Traders who operate with very tight profit targets often realize those targets sit too close to their cost floor. By slightly increasing minimum R targets, they give trades more room to absorb fees and still contribute positively to expectancy. This usually leads to fewer scratches and fewer “green but meaningless” wins.

Frequency naturally adjusts as a result of these changes. Traders stop taking trades out of boredom or habit. They become more aware of when the market environment justifies paying costs. Over time, trade counts drop, but decision quality improves.

Importantly, these adjustments come from data, not discipline slogans. The trader is not “being more patient” in the abstract. They are responding to concrete evidence that certain behaviors do not survive fees.

This is where many traders regain confidence. Instead of feeling like the market is random or unfair, they see clear cause-and-effect relationships in their data. Fees stop being an annoyance and start being a guide.

When your review process shows you exactly where costs hurt and where they do not, improvement becomes targeted and repeatable. That is when performance stops feeling fragile and starts feeling earned.

The Shift That Turns the Strategy Net-Positive (Case Study, Part 3)

The trader makes a few targeted adjustments. They raise minimum target thresholds so that marginal trades are filtered out. They stop chasing entries during the most chaotic moments. They experiment with passive orders in slower conditions. Trade frequency drops to around 150 per month.

The result is not dramatic at first. Gross PnL is slightly lower. But net performance improves. Expectancy turns positive. The equity curve becomes less noisy and more directional.

The key lesson is not “avoid scalping” or “trade less.” It is that fees define the minimum edge you need. If your strategy operates too close to that line, it will feel profitable while quietly bleeding.

Until this trader reviewed performance after fees, they were optimizing the wrong variables. Once costs were made visible, the path forward became clearer.

How Fees Stop Being a Mystery and Start Being a Constraint

Fees are not the enemy. They are a constraint.

Every viable strategy operates within boundaries. In crypto day trading, fees define one of the most important ones. They set the minimum edge you need for your execution style, frequency, and market environment. When you ignore them, you end up misreading your own performance.

Most traders who struggle here are not reckless. They are often disciplined, structured, and genuinely improving. The problem is that they are evaluating themselves using incomplete data. Gross results make them feel close. Net results tell the truth.

Once fees are treated as part of the system, clarity follows. You stop chasing tiny wins that do not matter. You stop blaming the market for flat equity. You start making changes that actually move the needle.

This is why serious traders track fees explicitly and review them in context. Not as a monthly expense, but as a performance variable tied to setups, sessions, and execution choices. When that information is always available in your journal, patterns surface faster and decisions get sharper.

A platform like TradeChainly makes this process easier by keeping fees attached to every trade and reflected in your metrics automatically. That removes guesswork and allows you to focus on analysis instead of reconstruction.

If your edge feels real but your account does not reflect it, look at fees first. Not emotionally. Not theoretically. In your data.

When you do, you often find that the problem is not your strategy. It is that you have been measuring the wrong version of it.