Building Clarity Before You Scale Risk

Why do you trade worse right after a hot streak?

There is a question most crypto traders delay asking for far too long.

Are my results coming from actual skill, or am I just running hot?

It sounds simple, but it is uncomfortable in a way few other questions are. As long as your PnL is green, it is easy to assume progress. A few strong weeks. A string of clean scalps on BTC or ETH. One breakout day that covers several small losses. Confidence creeps in quietly, backed by screenshots and account balance changes.

Crypto makes this illusion especially convincing. Leverage magnifies outcomes. Volatility creates fast feedback. You can feel like you “figured something out” after a handful of sessions. The market rewards aggression just often enough to reinforce it. When you are wrong, liquidation or a sharp drawdown feels like bad luck rather than a structural issue.

Luck is unavoidable in trading. The danger is mistaking short-term variance for repeatable edge, then scaling risk on top of it. That is how traders go from feeling consistent to wondering what went wrong in a matter of weeks.

Crypto day trading raises the stakes compared to slower markets. You are exposed to constant regime shifts. Funding flips. Liquidity thins on weekends. Volatility expands without warning. A strategy that looks brilliant across twenty trades can collapse across the next fifty if it is not grounded in something repeatable.

Most traders avoid this question because answering it honestly requires data, not feelings. It requires looking past your best days and studying what actually repeats when conditions change. It means accepting that some of your best trades may have been lucky, and some of your worst days may have been statistically normal.

Separating skill from luck is not about humility or mindset. It is a survival skill. Without it, you are always one hot streak away from overconfidence and one cold streak away from self-doubt. With it, you gain something far more valuable than confidence. You gain clarity.

Trading in crypto blurs that line faster than most markets.

Part of it is structural. The market never closes. There is no clean separation between sessions, no forced downtime to reset, and no natural pacing like you see in equities. You can trade Asia, Europe, and US hours in a single day, stacking exposure across very different liquidity and volatility conditions without realizing it.

Volatility is the second accelerant. Crypto does not move in smooth distributions. It compresses, then explodes. Liquidation cascades push price far beyond technical levels. Stops get skipped, targets get overfilled, and trades that should have been average suddenly look brilliant. When that happens a few times in a row, it is easy to credit skill when you were mostly on the right side of momentum.

Leverage adds another distortion. A small edge, or even no edge at all, can look impressive when 10x or 20x leverage turns noise into meaningful PnL. The problem is that leverage does not discriminate. It magnifies randomness just as efficiently as it magnifies precision. A trader can be net profitable for weeks while still having negative expectancy under the hood.

Funding rates add a layer most traders underestimate. In strong trends, funding can quietly eat into returns or inflate losses, especially for traders holding positions longer than planned. Two traders can take nearly identical setups on different exchanges and walk away with meaningfully different results simply due to funding mechanics and fee structures.

Exchange differences matter more than many want to admit. Binance often offers deeper liquidity and tighter spreads on majors. Bybit and OKX can behave differently during fast moves. Coinbase futures have their own quirks. A strategy that works cleanly on one venue can degrade on another without obvious changes to execution.

Put together, short-term results become a weak signal of skill. Crypto rewards being present during the right conditions as much as it rewards good decision-making. When conditions shift, luck evaporates quickly, and only structure remains.

Traders who rely on feel or recent PnL often swing between confidence and confusion. They are reacting to market noise rather than measuring performance across changing conditions. In crypto, the line between skill and luck is thin, and it moves constantly. Without a way to anchor your evaluation in data, you are always guessing where that line actually is.

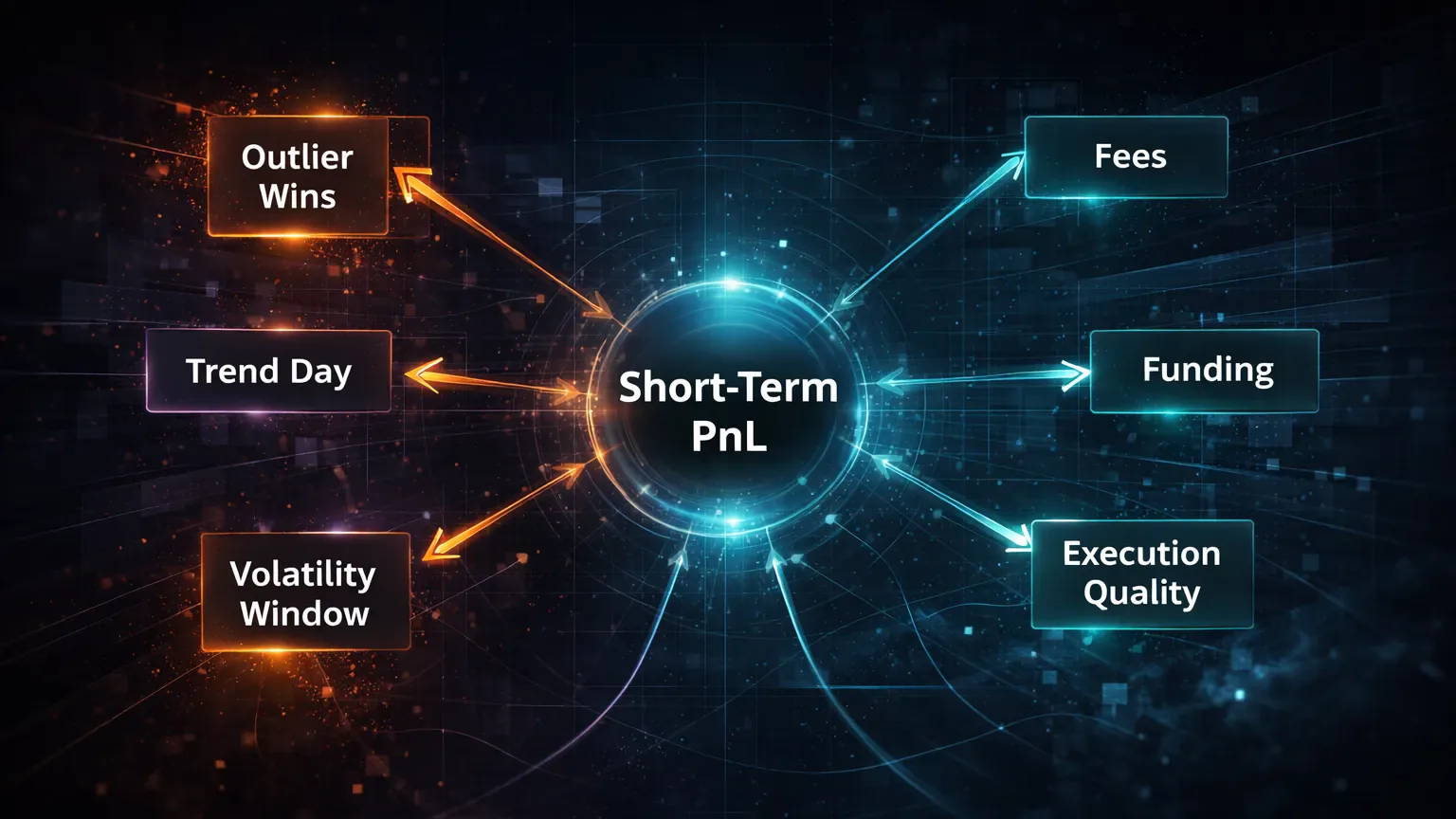

Stopping Short-Term PnL from Lying to You

Profit and loss feels like the most obvious scorecard in trading. You make money, something must be working. You lose money, something must be broken. In crypto day trading, that logic breaks down faster than most traders expect.

Short-term PnL is dominated by variance. A small sample of trades is easily distorted by one strong trend day, one liquidation sweep, or one oversized winner that masks a series of weak executions. Ten or twenty trades tell you almost nothing about whether your decisions have an edge. They mostly tell you whether the market cooperated.

Many traders get trapped here. They tweak a strategy, see immediate improvement, and assume causation. In reality, they may have simply aligned with a favorable volatility window. When conditions normalize, results revert, and confusion sets in.

Win rate is especially misleading in crypto. High win rates often come from tight targets and loose stops, or from trading during momentum bursts that do not last. A trader can win 70 percent of the time and still bleed slowly once fees, funding, and occasional large losses are factored in. Another trader can win less than half their trades and still be consistently profitable due to better risk and trade selection.

Even a run of green days does not guarantee progress. Many traders have experienced a strong first month after changing size or frequency, only to give it back over the next two. The early gains feel validating. The drawdown feels personal. Neither tells the full story on its own.

Crypto’s pace accelerates these misreads. You can accumulate dozens of trades in a short period, which creates the illusion of statistical significance. In reality, those trades may all belong to the same market regime. When volatility shifts or liquidity thins, the same approach produces very different outcomes.

Experienced traders stop using short-term PnL as their primary feedback loop. It is not that PnL does not matter. It is that it must be interpreted in context. Without separating what repeated well from what simply worked once, PnL becomes noise disguised as signal.

If you want to know whether skill is developing, you need metrics that survive changing conditions. You need to look beneath the surface of results and ask whether your decisions produce similar outcomes over time, not just during favorable stretches.

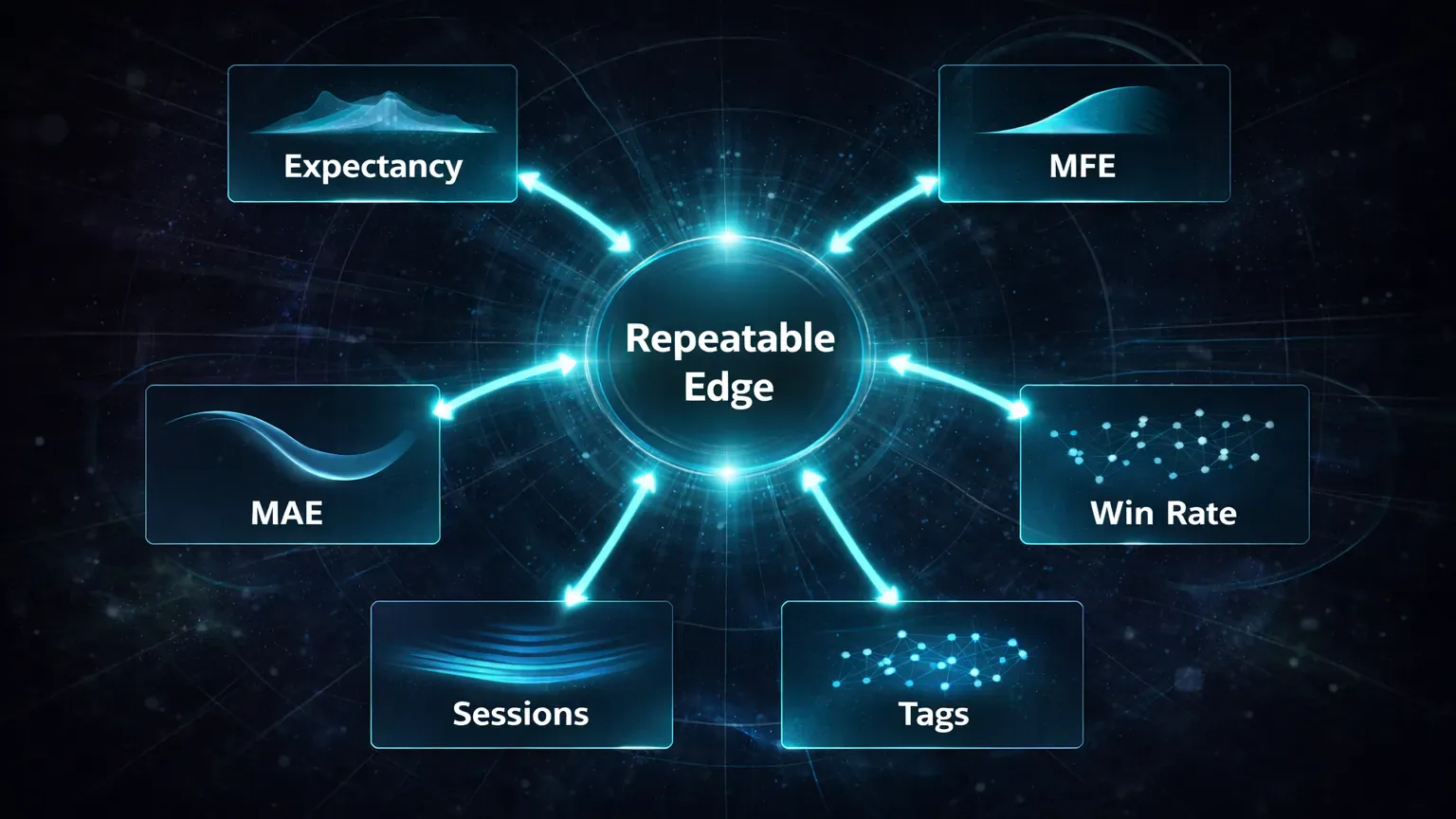

Measuring What Actually Repeats

If PnL and win rate are unreliable judges, the question becomes what actually works. The answer is not a single metric, but a small set of measurements that reveal whether your decisions hold up across time and conditions.

Expectancy sits at the center of this. It answers a simple but uncomfortable question. On average, does each trade you take make or lose money once everything is included. Fees, funding, partial exits, and occasional large losses all count. A trader with positive expectancy is not dependent on being right often. They are dependent on their process producing favorable outcomes over many repetitions.

In crypto, expectancy often tells a very different story than raw PnL. Many traders discover that their best-looking weeks came from negative expectancy masked by one or two outsized winners. Once those are removed, the remaining trades quietly bleed. Others find the opposite. Modest PnL hides a solid expectancy that improves dramatically once sizing and frequency are adjusted.

MAE and MFE add another layer of clarity. Maximum adverse excursion shows how far price moved against you before the trade worked or failed. Maximum favorable excursion shows how much you left on the table. Together, they expose execution quality in a way PnL never can. Consistently large MAE on winners often points to late entries or poor stop placement. Consistently small MFE on losers suggests exits driven by fear rather than structure.

Session-based performance is another filter that separates luck from skill. Many crypto traders perform well during specific hours without realizing it. Liquidity, volatility, and participation change dramatically between Asia, Europe, and US sessions. If your edge only exists during one window, mixing sessions in your analysis hides that reality.

Tag-level data is where patterns become undeniable. When you tag trades by setup, mistake, or emotional state, repeatability becomes visible. A setup that performs well across different weeks and market conditions is far more likely to represent skill. One that only works during explosive days is often luck wearing a convincing disguise.

This combination of metrics does not eliminate randomness. It contextualizes it. Instead of asking whether you are profitable this week, you start asking whether your behavior produces favorable statistics over time. That shift is what allows traders to scale with confidence rather than hope.

Turning a Hot Streak Into Repeatable Edge

Consider a trader who focuses on SOL and ETH perpetuals, primarily scalping five-minute breakouts during the US session. After a slow start to the quarter, they hit a strong run. Three weeks of clean execution. Multiple trend days. A handful of trades that run far beyond the initial target. The equity curve looks healthy, and confidence follows.

Naturally, size increases. Trade frequency creeps up. What felt controlled now feels efficient.

When the trader finally reviews the data in detail, the picture shifts. Expectancy across the full sample is barely positive. Nearly all the profit came from four trades taken during high-volatility trend days. The remaining trades are close to breakeven or slightly negative once fees and funding are included.

MAE tells a similar story. Many winning trades moved deep into drawdown before resolving. The trader often entered late, chasing confirmation rather than structure. Those trades happened to work during strong momentum, but the risk profile was poor. On quieter days, the same behavior produced stop-outs.

Session analysis adds another insight. Performance during the core US equity overlap was solid. Trades taken late in the session, especially during lower liquidity, consistently underperformed. The trader had been mixing these together and assuming the average reflected skill.

Tagging makes the final issue obvious. One specific breakout pattern shows consistent performance across weeks. Another setup, which felt intuitive and familiar, only worked during extreme volatility. It was not an edge. It was timing luck.

The trader adjusts. They reduce size until expectancy improves. They limit trading to the session where results are repeatable. They drop the volatile setup entirely and refine entries on the remaining one, using MAE data to tighten risk.

Over the next hundred trades, the curve smooths out. Fewer big days. Fewer emotional swings. The PnL grows slower but steadier. More importantly, the trader understands why.

This is what separating skill from luck looks like in practice. It is not dramatic. It is not motivational. It is a quiet shift from reacting to outcomes toward trusting repeatable behavior.

Building a Journal Review Loop That Exposes Variance

Understanding the difference between skill and luck only matters if it changes how you review your trading. Many traders stall here. They know what to look for in theory, but their review process still revolves around days, not decisions.

A useful workflow starts by stepping away from daily PnL summaries. Days mix too many variables together. Market regime, session, mood, and randomness all collide in a single number. Reviewing by trade and by tag forces separation. You begin to see which behaviors repeat and which only appear when conditions are unusually favorable.

Tagging is the backbone of this process. When trades are tagged by setup, mistake, and emotional state, performance becomes attributable. A losing day made up of high-quality executions looks very different from one driven by impatience or overtrading. Over time, the data makes this distinction obvious without interpretation.

Session filters add another layer. Reviewing results by Asia, Europe, and US sessions often reveals edges hiding in plain sight. Many traders discover they are consistently profitable during one window and consistently average or negative during others. Without separating sessions, luck masks this imbalance.

Metrics like MAE and MFE turn vague feelings into concrete signals. Instead of thinking you “often give trades too much room,” you can see exactly how far price moves against you before working. Instead of assuming you exit too early, you can quantify how much favorable movement you routinely leave unrealized. These patterns persist even when PnL fluctuates.

Automation matters because manual collection is tedious, which is why most traders never do it consistently. A journal that continuously imports trades and aggregates metrics makes long-term review realistic. Tools like TradeChainly exist to remove friction from this process, not to replace judgment, but to make objective evaluation possible without spreadsheets.

When your workflow is built around repeatable behaviors instead of daily outcomes, luck loses its grip. Good days feel normal. Bad days feel informative. Over time, skill stops being something you guess at and becomes something you can verify.

Stress-Testing Your Edge with Simple Checks

Once you understand what separates skill from luck conceptually, the next step is pressure-testing your own results. Not with opinions or narratives, but with simple checks that expose whether your edge survives scrutiny.

Start with sample size discipline. Fewer than fifty trades tells you very little, especially in crypto. A hundred trades begins to reveal structure. Two hundred or more starts to show whether results persist across different volatility regimes. If your confidence depends on a small cluster of trades, assume luck until proven otherwise.

Next, remove outliers and reassess. Strip out your single best day or two. Recalculate expectancy without them. If your performance collapses, those days were carrying your results. Skill should survive the loss of outliers. Luck usually does not.

Compare tagged setups against each other instead of against your total PnL. One setup performing consistently across weeks and conditions is meaningful, even if it is not flashy. Another that only performs during extreme momentum is informational, but it should not be trusted as a foundation. This comparison is where many traders realize they are trading too many ideas at once.

Session testing is equally revealing. Segment your data by trading hours and review expectancy, MAE, and win rate separately. If your edge only exists during one window, trading outside of it is not diversification. It is dilution.

Finally, check stability over time. Does expectancy improve as you gain experience, or does it oscillate wildly? Does MAE shrink as entries refine, or stay erratic? Skill leaves fingerprints. Luck leaves noise.

None of these tests are complicated. What makes them powerful is repetition. Running them regularly turns performance review into a process instead of a reaction. Over time, the question of skill versus luck stops being emotional. The data answers it for you.

Trading Like Skill, Not Like Noise

Luck announces itself loudly in crypto. It shows up as oversized winners, sudden confidence, and the feeling that you finally synced with the market. Skill, by contrast, is quiet. It looks like similar trades producing similar outcomes across weeks that feel very different emotionally.

So many traders chase excitement in their results. Loud outcomes feel meaningful. Smooth performance feels underwhelming. Over time, this bias pushes traders toward behaviors that look impressive short term and fail under pressure.

Separating skill from luck flips that instinct. You stop judging progress by how big your best day was and start judging it by how stable your metrics remain when conditions change. You become less reactive to swings and more attentive to patterns.

Crypto rewards this mindset more than most markets. Volatility is unavoidable. Funding and fees never stop. Liquidity shifts constantly. Without a way to anchor your evaluation in data, confidence is fragile. With it, confidence becomes proportional to evidence.

A solid journaling process does not eliminate randomness. It makes randomness visible. When you can see which behaviors repeat and which only appear during favorable conditions, decision-making gets simpler. You trade less, but with more intent. You size with restraint. You review without defensiveness.

Tools like TradeChainly fit naturally into a serious trader’s workflow. Not as a shortcut to profitability, but as infrastructure. By automating trade collection and surfacing the metrics that matter, it allows you to focus on improving execution rather than debating outcomes.

In the long run, the traders who survive are not the ones with the loudest results. They are the ones who can tell the difference between noise and edge, then act on that distinction consistently.